Insuring Against Economic Downturns & Recessions

Economic slowdowns and recessions pose considerable challenges for companies. In addition to the potential for decreased revenues, increased costs, and declining valuations, companies will encounter additional turbulence as the potential for litigation, occupational fraud and cyber-attacks all increase. In an effort to reduce costs, many companies may decide to reduce or eliminate insurance coverage, however this approach may adversely impact an organization’s total cost of risk. A strong executive & management liability insurance portfolio serves a critical role in protecting the corporate entity, its balance sheet, and c-suite, particularly during economic downturns.

DIRECTORS & OFFICERS INSURANCE: It’s a domino effect; the economy slows down, companies suffer, stakeholders suffer…stakeholders sue. In an effort to recoup any financial losses sustained, investors and creditors of failed or failing companies will carefully scrutinize the activities that resulted in their losses, and may pursue actions against the company’s corporate officers. Often these lawsuits will assert some element of fraud or breaches of fiduciary duties, alleging wrongdoing such as misappropriation of corporate assets, or materiel misrepresentations in financial statements. Even absent any clear wrongdoing, claims may be brought without merit, inflicting significant defense costs upon the company, and/or its directors and officers. Being that automatic stays generally do not provide protection to corporate officers, and being that corporate veils can be breached, executives sitting on uninsured (or underinsured) companies may find themselves with little or no protection, with their personal assets effectively exposed as they are forced to fund their own defense and may be held personally liable for any resulting damages awarded by the courts. When the corporate entity is insolvent and indemnification is unavailable, the only protection during such litigation is the Side A insuring agreement of a D&O policy which will extend coverage for defense costs (and potentially settlements) when directors or officers are named as individual defendants. Additionally, D&O insurance serves a valuable role in keeping a company’s balance sheet strong, potentially helping to avoid insolvency altogether, by providing coverage for covered claims against the entity and indemnifiable claims against its executives. A hypothetical claim amounting to 3 Mill in defense costs and an 8 Mill settlement could inflict significant damage to a company’s already distressed balance sheet – damage that could otherwise have been avoided by tendering the claim to the insurer.

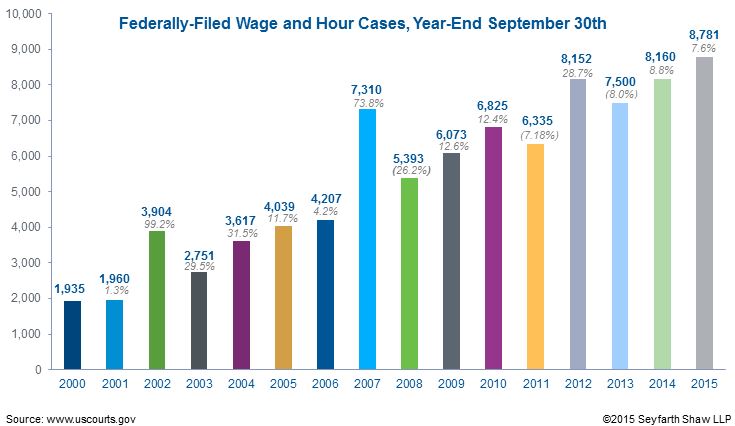

EPLI INSURANCE: Faltering economies also give rise to employment related lawsuits. A report by Nera Consulting estimates that wrongful discharge claims alone increased 21% during the last recession when compared to prior years. Employees pursuing wrongful termination claims may also allege a wider range of wrongful acts. Employees that have sustained (and ignored) prior workplace misconduct such as discrimination or harassment, may decide to bring that conduct forward upon being terminated. During downsizing, older employees that are terminated will also encounter difficulties when attempting to locate new employment, resulting in an increase in age discrimination claims. In fact, 2008 still remains the single largest year in the past 20 years for age discrimination claims filed with the EEOC. Frivolous claims are also likely to increase as employees become desperate. The first wave of claims however may arrive in the form of allegations of wage and hour violations. According to data compiled by Seyfarth Shaw, 2007 (the year the economy began its downward slope) saw a significant spike in wage and hour violations.

{kind=link}

In addition to an increase in claim frequency, the same report by Nera Consulting (above) highlights that recessions may also increase claim severity due to an increase in calculated plaintiff damages resulting from depressed wages and the lengthy time required to locate new employment. Employers believing they are protected by “employment at will”, should be aware that employment at will doctrines may reduce (but do not eliminate) the risk of wrongful termination claims.

CRIME INSURANCE: There has always been an inverse relationship between the economy and crime rates. As the economy becomes more distressed, crimes increase, and vice versa. Workplace crime and fraud are no exception. As employee’s encounter financial pressure and rising debt, they are more likely to commit workplace fraud, namely employee embezzlement. Additionally, aggrieved employees that are let go during downsizing, may feel as though they are being unfairly targeted, and retaliate by committing theft prior to their departure. A survey conducted by the association of certified fraud examiners during the 2008 recession highlights the true extent of the increase in occupational fraud. Of the respondents used for the survey:

- 28% indicated the number of claims were approximately the same, while 55% observed an increase in claim frequency

- 28% indicated the value of frauds remained approximately the same, while ~ 50% observed an increase in claim severity

- 88% believed occupational fraud would continue to increase over the following year

- Per a separate ACFE report (here), the median loss amounts for 2018 were $130k, with 22% of cases causing losses in excess of $1 Million

These statistics underscore the importance of crime insurance. Companies operating without such coverage will have no source of recovery when theft and fraud are ultimately discovered, inflicting additional stress to an already distressed balance sheet. In order to further mitigate the risk of occupation fraud, companies should also ensure their internal controls, policies and procedures are as strong as possible. This should include, among other policies, a review of internal audit procedures, segregation of duties, mandatory vacations, and employee training.

CYBER INSURANCE: According to FBI’s internet crime complaint center, there were a total of 351k complaints in 2018. The second largest year? 2009, the year of the last recession, with 336k complaints. This surge can likely be attributed to a number of factors. During economic downturns, there appears to be an increase in the number of malicious actors – these include domestic and foreign cyber criminals along with rogue/aggrieved employees such as terminated IT personnel. Additionally, as employees become stressed and overworked, and companies attempt to reduce costs and cut corners, the quality of cyber security will decrease. As a result, cyber criminals are likely to exploit these new vulnerabilities with greater efficiency, employing targeted social engineering (CEO Fraud) campaigns and ransomware attacks, among others. When a corporate balance sheet is already stressed, cyber intrusions and even privacy events stemming from human error have the ability to tip a company over the edge forcing it into insolvency. AMCA, Little and King and Altegrity are just 3 examples of companies that were ultimately forced into bankruptcy following cyber security related events. While cyber insurance cannot provide complete, failsafe protection against any and all risk, a carefully tailored policy can provide coverage for most of the claims an organization may encounter, helping to keep the company’s balance sheet healthy.

TRADE CREDIT INSURANCE: “You’re only as strong as your weakest link” - the same holds true for corporate financials. Accounts receivables are a main asset for many companies - an inability to collect those receivables is effectively a lost asset, which can severely strain a company’s balance sheet. As clients and customers encounter financial challenges of their own, the risk of default increases. While it may not fall under the umbrella of executive and management liability insurance, trade credit insurance is an equally critical component of a well-rounded insurance portfolio during economic instability. Also known as accounts receivable insurance, it provides balance sheet protection by reimbursing a corporate entity for losses sustained due to an inability to collect its own receivables. This may stem from client/customer insolvency, or simple refusal to pay, both of which would qualify as covered losses under most trade credit policies (as long as the client is not citing defective products or services).

Many companies understandably decide to cut costs during economic downturns, with insurance premiums being a common target for cost reduction. This is particularly true when policyholders experience steadily increasing premiums despite their revenues decreasing. Additionally, premiums may further inflate during recessions, as insurers attempt to offset losses or adjust policyholder premiums based on specific underwriting criteria such as weakened financials, layoffs, or recent losses. Reducing or eliminating insurance however (particularly management and executive liability) is shortsighted. Emphasizing a marginal cost savings over insurance coverage, while ignoring the relative increase in exposures during an economic downturn, can result in absorbing losses that can greatly exceed any amounts saved. Recessions are in fact the time companies should pay greater attention to the adequacy of policy limits and depth of coverage. For companies that have no such insurance in force and are seeking first time placements, it is best advised to place these in advance, while your company is performing well. Attempting to place coverage when financials begin to decline, or following significant events such as recent losses or layoffs will only be perceived as efforts to cover the proverbial burning building, resulting in difficult placements.

Get (Risk) Managed.

Ready to review your existing insurance program? Interested in setting a reminder for a renewal review? Or simply have a question? We're here to help. We also understand you're busy - let's schedule a time to speak that works best for you. Simply schedule a call and we'll reach out when it's convenient.